Substation Relay Protection Training

Our customized live online or in‑person group training can be delivered to your staff at your location.

- Live Online

- 12 hours Instructor-led

- Group Training Available

Regular Price:

$699

Coupon Price:

$599

Is it legal for a Public Service Company of New Mexico customer to buy renewable energy from someone else?

The question has been a matter of growing debate between renewable-energy advocates and the state's three main utility companies, including PNM.

Utilities have argued that allowing third parties, such as a solar-energy company, to install a system, hook into the power grid and collect money from one of the utility's customers would infringe on the utility company's franchise rights. Power companies like PNM, which provides electricity to Santa Fe and other parts of north-central New Mexico, contend state law prohibits other energy providers from poaching on their service territories.

The New Mexico Public Regulation commission decided during a public meeting to have a hearing examiner accept legal briefs on the question, PRC commissioner Jason Marks said.

The commission will review the briefs before making a ruling.

Marks said the issue arose two years ago, after the PRC required utilities by 2011 to diversify their sources for meeting the state's renewable energy standard. State law requires utilities such as PNM to provide a portion of electricity from renewable sources. Marks said utilities had relied largely on large-scale wind farms to meet the standard.

Now the PRC requires utilities to have a certain percentage of renewable energy also come from utility-scale solar installations and from "distributed sources." Distributed sources can include utility customers who install rooftop solar panels or put wind generators in yards.

The city of Santa Fe is looking at installing a solar photovoltaic system to produce some of its own power and offset its monthly energy bill from PNM. That system would be owned by another company.

Related News

'That can keep you up at night': Lessons for Canada from Europe's power crisis

Canada Net-Zero Grid Lessons highlight Europe's energy transition risks: Germany's power prices, wind and solar…

View more

GM president: Electric cars won't go mainstream until we fix these problems

Electric Vehicle Adoption Barriers include range anxiety, charging infrastructure, and cost parity; consumer demand, tax…

View more

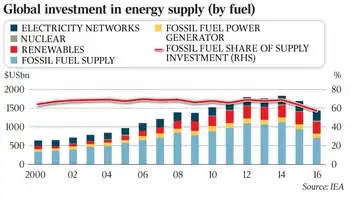

IEA warns fall in global energy investment may lead to shortages

Global Energy Investment Decline risks future oil and electricity supply, says the IEA, as spending…

View more

Solar power growth, jobs decline during pandemic

COVID-19 Solar Job Losses are erasing five years of workforce growth, SEIA reports, with U.S.…

View more

Power bill cut for 22m Thailand houses

Thailand Covid-19 Electricity Bill Relief offers energy subsidies, tariff cuts, and free power for small…

View more

Reliability of power winter supply puts Newfoundland 'at mercy of weather': report

Labrador Island Link Reliability faces scrutiny as Nalcor Energy and General Electric address software issues;…

View more

Sign Up for Electricity Forum’s Newsletter

Stay informed with our FREE Newsletter — get the latest news, breakthrough technologies, and expert insights, delivered straight to your inbox.

Electricity Today T&D Magazine Subscribe for FREE

Stay informed with the latest T&D policies and technologies.

- Timely insights from industry experts

- Practical solutions T&D engineers

- Free access to every issue