NFPA 70E Training

Our customized live online or in‑person group training can be delivered to your staff at your location.

- Live Online

- 6 hours Instructor-led

- Group Training Available

Regular Price:

$199

Coupon Price:

$149

TORONTO

—

Hydro One Account Customization lets Ontario customers pick billing due dates, enable balanced billing, get early high usage notifications, monitor electricity consumption, and receive outage alerts, offering flexibility during COVID-19.

Story Summary

A flexible toolkit to set due dates, balance bills, get usage alerts, and track electricity.

Pick your own billing due date to match cash flow

Balanced billing smooths seasonal peaks from AC and heating

Ultra-Low Overnight Price Plan encourages off-peak energy use

Early high-usage notifications help you track consumption

Report outages online and get text or email restoration alerts

Hydro One announced it is providing its customers with the flexibility to customize their account. Customers can choose their own billing due date, flatten usage spikes from temperature fluctuations through balanced billing and the Ultra-Low Overnight Price Plan, and monitor their electricity consumption by signing up for early high usage notifications.

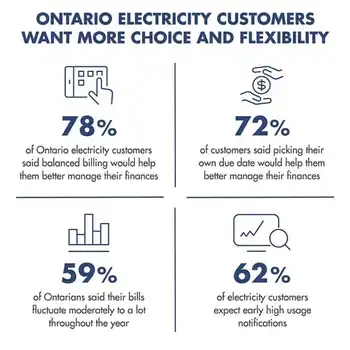

Research shows that Ontario electricity customers want more choice and flexibility (CNW Group/Hydro One Inc.)

"Being in-tune with our customers' needs is more important than ever. As we continue to navigate the COVID-19 pandemic, customers tell us that choice and flexibility, alongside electricity relief, will help them during this difficult time," said Jason Fitzsimmons, Chief Corporate Affairs and Customer Care Officer, Hydro One. "As a customer-driven organization, we have an important responsibility to support customers with relief, flexibility and choice."

According to recent research conducted by Angus Reid, 78 per cent of Ontario electricity customers said balanced billing would help them better manage their finances, even as peak hydro rates remained unchanged for many self-isolating customers. Balanced billing flattens out the spikes in electricity usage that commonly occurs in the summer due to air conditioning use and in the winter due to heating.

The research also found that 72 per cent of customers would like to pick their own due date to better manage their finances. This feature is now included in Hydro One's new customization bundle, which will be shared with customers through an awareness campaign. Other customization tools include alerts when electricity usage falls outside of the customer's normal pattern, the ability to report outages online and the ability to receive text messages or emails when outages occur. Customers can visit www.HydroOne.com/Choice to learn more.

"Customers can pick and choose the tools that work best for them. We are now able to offer a suite of features built for any lifestyle as our employees support Ontario's COVID-19 response across the province," said Fitzsimmons.

In addition to these customization options, Hydro One has also developed a number of customer support measures during COVID-19, including a Pandemic Relief Fund to offer payment flexibility and financial assistance to customers. The company is also extending its ban on electricity disconnections to ensure that no customer is disconnected at a time when support is needed most. More information about Hydro One's Pandemic Relief Program can be found at www.HydroOne.com/PandemicRelief. Customers can continue to contact Hydro One to determine individual payment plans and determine financial assistance programs available to meet their needs, especially as disconnection pressures can arise for some households.

Related News

Related News

Cleaning up Canada's electricity is critical to meeting climate pledges

Canada Clean Electricity Standard targets a net-zero grid by 2035, using carbon pricing, CO2 caps,…

View more

Ontario's five largest electricity providers join together to warn of holiday scams

Ontario Electricity Bill Scams: beware phishing, spoofed calls, fake invoices, and disconnection threats demanding prepaid…

View more

Sen. Cortez Masto Leads Colleagues in Urging Congress to Support Clean Energy Industry in Economic Relief Packages

Clean Energy Industry Support includes tax credits, refundability, safe harbor extensions, EV incentives, and stimulus…

View more

Winter Storm Leaves Many In Texas Without Power And Water

Texas Power Grid Crisis strains ERCOT as extreme cold, ice storms, and heavy snow trigger…

View more

Price Spikes in Ireland Fuel Concerns Over Dispatachable Power Shortages in Europe

ISEM Price Volatility reflects Ireland-Northern Ireland grid balancing pressures, driven by dispatchable power shortages, day-ahead…

View more

To Limit Climate Change, Scientists Try To Improve Solar And Wind Power

Wisconsin Solar and Wind Energy advances as rooftop solar, utility-scale farms, and NREL perovskite solar…

View more

Sign Up for Electricity Forum’s Newsletter

Stay informed with our FREE Newsletter — get the latest news, breakthrough technologies, and expert insights, delivered straight to your inbox.

Electricity Today T&D Magazine Subscribe for FREE

Stay informed with the latest T&D policies and technologies.

- Timely insights from industry experts

- Practical solutions T&D engineers

- Free access to every issue