NFPA 70b Training - Electrical Maintenance

Our customized live online or in‑person group training can be delivered to your staff at your location.

- Live Online

- 12 hours Instructor-led

- Group Training Available

Regular Price:

$699

Coupon Price:

$599

BC Hydro Kamloops Substation will expand grid capacity to meet rising electricity demand, support population growth in the southwest, and enhance reliability with new transmission links, modern infrastructure, and lower environmental and archaeological impacts.

What's Happening

A $49M BC Hydro project near Bunker Road to boost grid reliability and capacity for Kamloops' growing southwest by 2018.

- Construction starts fall 2016; in service expected 2018.

- $49 million investment aligned with BC Hydro capital plan.

- Sited off Bunker Road, near Kenna Cartwright Park.

BC Hydro and the City of Kamloops have reached an agreement for BC Hydro to acquire land from the city for the construction of a new substation in southwest Kamloops. The substation is needed to help meet growing electricity demand.

"BC Hydro is projecting electricity demand to increase by about 30 over the next 10 years alone," said Todd Stone, MLA, Kamloops-South Thompson. "Electricity is the backbone of our economy and essential to our way of life. A growing city needs power and this new substation will help to ensure that reliable power is there when we need it."

The new substation for BC Hydro will be built on an industrial site off Bunker Road that is adjacent to the city works yard and Kenna Cartwright Park. The site is close to existing transmission lines and has low potential for environmental and archaeological impacts.

"Over the next 20 years, the population of the city is expected grow by 25 per cent," said Mayor Peter Milobar, City of Kamloops. "Much of this growth will be in the southwest area of Kamloops and we've been working closely with BC Hydro to identify a site for the new substation to ensure the electrical needs of the region are met, as vehicle electrification continues across B.C."

"The new substation in Kamloops is a key part of BC Hydro’s capital plan," said Chris O'Riley, Deputy CEO & Capital Infrastructure Project Delivery, BC Hydro. "BC Hydro is making significant investments in the province's generating stations and generation facilities, power lines and substations to help meet growing demand throughout B.C. This requires investing, on average, $2.4 billion a year, over the next 10 years, in B.C.'s electricity system."

Construction of the new substation is scheduled to begin in the fall of 2016 and the new substation is expected to be in service in 2018 to help deliver new power sources across the region. The cost of the project is estimated at $49 million. BC Hydro is currently working on substation design and will host an information session for the public later this year or early next year.

Related News

Related News

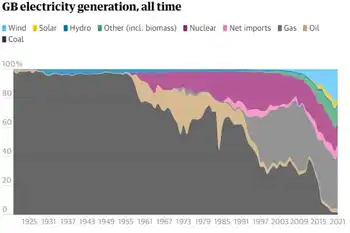

Energy dashboard: how is electricity generated in Great Britain?

Great Britain electricity generation spans renewables and baseload: wind, solar, nuclear, gas, and biomass, supported…

View more

Canadian Electricity Grids Increasingly Exposed to Harsh Weather

North American Grid Reliability faces extreme weather, climate change, demand spikes, and renewable variability; utilities,…

View more

Southern California Edison Faces Lawsuits Over Role in California Wildfires

SCE Wildfire Lawsuits allege utility equipment and power lines sparked deadly Los Angeles blazes; investigations,…

View more

California's solar energy gains go up in wildfire smoke

California Wildfire Smoke Impact on Solar reduces photovoltaic output, as particulate pollution, soot, and haze…

View more

BOE Says UK Energy Price Guarantee is Key for Next Rates Call

UK Market Stability Outlook remains febrile as the Bank of England, Treasury, and OBR forecasts…

View more

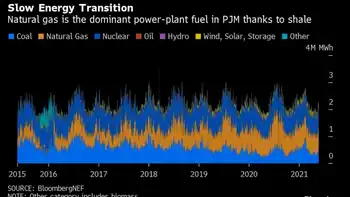

Electricity Payouts on Biggest U.S. Grid Fall 64 Per Cent in Auction

PJM Capacity Auction Price Drop signals PJM Interconnection capacity market shifts, with $50/MW-day clearing, higher…

View more

Sign Up for Electricity Forum’s Newsletter

Stay informed with our FREE Newsletter — get the latest news, breakthrough technologies, and expert insights, delivered straight to your inbox.

Electricity Today T&D Magazine Subscribe for FREE

Stay informed with the latest T&D policies and technologies.

- Timely insights from industry experts

- Practical solutions T&D engineers

- Free access to every issue