Protective Relay Training - Basic

Our customized live online or in‑person group training can be delivered to your staff at your location.

- Live Online

- 12 hours Instructor-led

- Group Training Available

Regular Price:

$699

Coupon Price:

$599

Global demand for coal has shown some signs of slack, leaving investors to wonder what's next for U.S. producers who've seen prices at times triple over the past year.

Ocean freight rates, the U.S. dollar and other factors behind the big jump have begun to ease. Meanwhile, analysts are questioning whether a global slowdown has begun to hurt the steel industry, which uses high-priced metallurgical coal to fire blast furnaces.

Investment bank Goldman Sachs downgraded the entire U.S. steel industry, citing risks such as the strengthening dollar and concerns about demand from China.

Shares in one of the biggest coal producers, Massey Energy Co. tumbled nearly 8 percent, or $4.37, to $51.40 recently on news that 2008 prices and production are showing signs of weakness.

St. Louis-based coal giant Peabody Energy offered a more bullish assessment during a presentation at a Lehman Brothers investor conference. Peabody, the world's largest privately held coal producer, said world coal demand continues to exceed supply and prices remain strong and rising.

Massey Chief Executive Don Blankenship said much the same thing: prices for metallurgical coal remain strong as demand continues to exceed supply. "Despite some of the more recent publications we find it to be extremely tight."

So tight, Blankenship said, that Massey has sold 7 million tons at an average price of $173 for 2009 and 2010 deliver.

"We will see coal prices in the $220 to $250 range," he said. "It could be higher. It will depend to a great extent again on what the Australians are doing and what the Chinese are doing."

While steam coal has slipped a bit — Central Appalachian coal for electric power plants closed at $105, down from $143 in July — Blankenship noted the price remains historically high.

Stifel, Nicolaus & Co. analyst Paul Forward blamed lower volumes of metallurgical coal for lukewarm 2008 price and production guidance issued by Richmond, Va.-based Massey in a report. Met coal has soared to $250 a ton at times this summer, from less than $100 a ton a year ago. As Forward notes, Massey's stock has fallen about 40 percent in the third quarter after jumping 157 percent in the second quarter.

Should steel prices wane and U.S. steel producers cut production, the run for coal companies may be coming to and end, at least for now. Common-grade scrap steel, for instance, has dropped from as much as $550 a ton to below $400, making steelmakers who use electric furnaces more competitive with mills that burn coal, said steel analyst Charles Bradford of Bradford Research/Soleil Securities.

"The met coal is typically tied to the production of steel and I think, over the short term, production of steel by the integrated steel mills is going to slow," he said. "They've got to reduce supply."

Just how that affects metallurgical coal demand and price is uncertain. International steel demand and production has remained relatively strong and China, a major importer, still faces a coal shortage, Bradford said.

Ocean freight rates have also helped push U.S. coal exports up an estimated 51 percent this year.

After doubling earlier this year, Bradford says freight rates have dropped more recently, though they remain higher than January's low point.

Related News

Turkish powership to generate electricity from LNG in Senegal

Karpowership LNG powership in Senegal will supply 15% of the grid, a 235 MW floating…

View more

Utility giant Electricite de France acquired 50pc stake in Irish offshore wind farm

Codling Bank Offshore Wind Project will deliver a 1.1 GW offshore wind farm off the…

View more

Seattle City Light's Initiative Helps Over 93,000 Customers Reduce Electricity Bills

Seattle City Light Energy Efficiency Programs help 93,000 residents cut bills with rebates, home energy…

View more

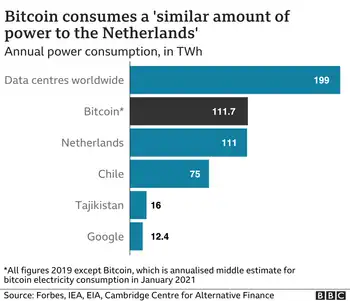

How Bitcoin's vast energy use could burst its bubble

Bitcoin Energy Consumption drives debate on blockchain mining, proof-of-work, carbon footprint, and emissions, with CCAF…

View more

B.C. Hydro misled regulator: report

BC Hydro SAP Oversight Report assesses B.C. Utilities Commission findings on misleading testimony, governance failures,…

View more

Bruce nuclear reactor taken offline as $2.1B project 'officially' begins

Bruce Power Unit 6 refurbishment replaces major reactor components, shifting supply to hydroelectric and natural…

View more

Sign Up for Electricity Forum’s Newsletter

Stay informed with our FREE Newsletter — get the latest news, breakthrough technologies, and expert insights, delivered straight to your inbox.

Electricity Today T&D Magazine Subscribe for FREE

Stay informed with the latest T&D policies and technologies.

- Timely insights from industry experts

- Practical solutions T&D engineers

- Free access to every issue