Substation Relay Protection Training

Our customized live online or in‑person group training can be delivered to your staff at your location.

- Live Online

- 12 hours Instructor-led

- Group Training Available

Regular Price:

$699

Coupon Price:

$599

The Sunflower Electric Power CorporationÂ’s proposal for a cleaner coal plant in southwest Kansas has been passed, according to Sunflower Electric.

Governor Mark Parkinson signed a renewable energy bill as part of his agreement to overcome the 19-month feud between Sunflower and the governor's office.

The new deal allows the construction of a coal-powered plant — though one much smaller than the original plans called for — outside of Holcomb, Kan. The bill also calls for renewable energy sources, like wind, to provide 20 percent of the public utilities' electricity by 2020.

ParkinsonÂ’s plan also includes updates for transmission lines. This will allow the current wind farms to tie in to the new system.

“We’re not going to be able to fully develop the wind capacity in Kansas unless we have transmission capability,” said House Speaker Mike O'Neal, R-Hutchinson.

According to a Sunflower press release, the corporation will be allowed to build an 895-megawatt plant, with enough storage to provide power to approximately 448,000 households. Sunflower agreed to work toward off-setting potential carbon-dioxide emissions, which are estimated to be 6.7 million tons per year.

Sunflower had applied for a permit in 2006 to build its plant with three generating units at 2,100 megawatts. They were denied early due to carbon emissions, and the company fought for two years at the state level before the agreement was reached.

The Environmental Protection Agency determined that too much about this project has been altered to allow Sunflower to move ahead with its initial permit, according to David Bryan, spokesman for the EPA's regional office in Kansas City.

“We believe the proposal by Sunflower is a new project,” Bryan said. “That means we expect a public comment period, a technical analysis, all the things that need to be done.”

Related News

NB Power launches public charging network for EVs

NB Power eCharge Network expands EV charging in New Brunswick with fast chargers, level 2…

View more

B.C.'s Green Energy Ambitions Face Power Supply Challenges

British Columbia Green Grid Constraints underscore BC Hydro's rising imports, peak demand, electrification, hydroelectric variability,…

View more

Electricity alert ends after Alberta forced to rely on reserves to run grid

Alberta Power Grid Level 2 Alert signals AESO reserve power usage, load management, supply shortage…

View more

'Unbelievably dangerous': NB Power sounds alarm on copper theft after vandalism, deaths

NB Power copper thefts highlight risks at high-voltage substations, with vandalism, fatalities, infrastructure damage, ratepayer…

View more

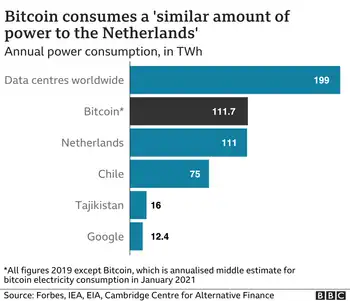

How Bitcoin's vast energy use could burst its bubble

Bitcoin Energy Consumption drives debate on blockchain mining, proof-of-work, carbon footprint, and emissions, with CCAF…

View more

Hitachi freezes British nuclear project, books $2.8bn hit

Hitachi UK Nuclear Project Freeze reflects Horizon Nuclear Power's suspended Anglesey plant amid Brexit uncertainty,…

View more

Sign Up for Electricity Forum’s Newsletter

Stay informed with our FREE Newsletter — get the latest news, breakthrough technologies, and expert insights, delivered straight to your inbox.

Electricity Today T&D Magazine Subscribe for FREE

Stay informed with the latest T&D policies and technologies.

- Timely insights from industry experts

- Practical solutions T&D engineers

- Free access to every issue