Substation Relay Protection Training

Our customized live online or in‑person group training can be delivered to your staff at your location.

- Live Online

- 12 hours Instructor-led

- Group Training Available

Regular Price:

$699

Coupon Price:

$599

Coal Plant Investment Risks encompass carbon regulation, cumulative compliance costs, credit rating scrutiny, and fuel volatility, demanding fuller bond disclosures as cleaner alternatives like natural gas, wind, solar, and energy efficiency undercut coal's competitiveness.

Main Details

Carbon rules, pollution, ash, fuel volatility, and cleaner rivals make coal risky, needing stronger bond disclosures.

- Federal RUS halts tax-backed coal plant financing as too risky

- Treasury offers no bondholder guidance on carbon-related exposures

- Moody's, S&P cite cumulative risk from overlapping regulations

- Costs include SO2, mercury, ash disposal, and volatile coal prices

- Gas, wind, solar, efficiency undercut coal; closures reflect economics

Andrew Ackerman's January 13 article "Climate Disclosure Sought" accurately reflects the current state of public debate on disclosure of financial risk to investors in tax-exempt bonds that support new and existing coal-fired electric generation plants. It is a debate fraught with paradox and risk.

Federal energy experts, the Rural Utility Service, have stopped allowing federal tax dollars to be invested in these coal plants because they are risky investments. In large measure this is due to impending costs imposed due to carbon pricing and new carbon regulations that are taking shape.

Federal finance experts at the Treasury Department have ignored this energy expertise and issued no guidance to bond investors, as if the risk to a federal tax dollar were somehow different than a bondholder's dollar.

Our credit rating agencies seem equally confused. In your article a representative of Moody's defends a recent bond disclosure for a new coal plant because the offering document contains some discussion of climate disclosure within the filing. The disclosure he defends ignores the same worrisome set of credit risks that Moody's warned about in February 2008 in a special report on climate risk.

Developers of coal plants and utilities face not only the risk of new carbon regulations and the costs from them, but they also face compliance costs with regard to sulfur dioxide, mercury and other air pollution requirements.

The recent ash spill in Tennessee has added future regulation of ash disposal onto the list of new costs. The volatility of future coal costs have been raised as a matter of concern by federal agencies as well.

Moody's and Standard & Poor's have raised the issue of "cumulative risk" in their reports. Future carbon regulation alone creates a significant financial risk to coal as a future resource for electricity generation. However, as a pure financial play it is the combination of regulatory burdens and shifting market realities related to coal generation, including CO2 storage liability considerations for sequestration projects, that requires a full explanation for investors.

The recent changes in the nation's fortunes related to its natural gas supply have placed the rising cost of coal into stark relief against its competition: wind, solar, natural gas and energy efficiency. Progress Energy's recent decision to close much of its existing coal fleet rests on its own cost-benefit analysis of these risks, echoing how investors pressed utilities to disclose climate risks across the sector.

Comprehensive disclosure of information to bond investors is essential to smooth market functioning. This needs to include untidy facts like the federal government pulling out of financing coal plants, and exceptions such as ongoing support for clean coal projects in limited cases, as well as disclosure of the cumulative costs from factoring the real cost of coal into the price of electricity, even if it shows that coal-plant investments are no longer competitive.

Related News

Blizzard and Extreme Cold Hit Calgary and Alberta

Calgary Winter Storm and Extreme Cold delivers heavy snowfall, ECCC warnings, blowing snow, icy roads,…

View more

Covid-19 puts brake on Turkey’s solar sector

Turkey Net Metering Suspension freezes regulator reviews, stalling rooftop solar permits and grid interconnections amid…

View more

Commission unveils Grids Package to speed transmission and distribution upgrades

European Grids Package sets out accelerated permits and digital tools to modernize transmission and distribution…

View more

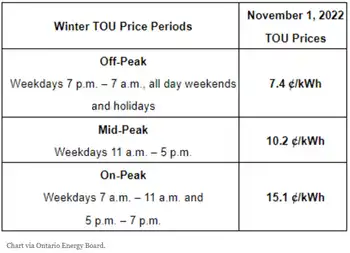

Electricity rates are about to change across Ontario

Ontario Electricity Rate Changes lower OEB Regulated Price Plan costs, adjust Time-of-Use winter hours and…

View more

Wartsila to Power USA’s First Battery-Electric High-Speed Ferries

San Francisco Battery-Electric Ferries will deliver zero-emission, high-speed passenger service powered by Wartsila electric propulsion,…

View more

Electricity use actually increased during 2018 Earth Hour, BC Hydro

Earth Hour BC highlights BC Hydro data on electricity use, energy savings, and participation in…

View more

Sign Up for Electricity Forum’s Newsletter

Stay informed with our FREE Newsletter — get the latest news, breakthrough technologies, and expert insights, delivered straight to your inbox.

Electricity Today T&D Magazine Subscribe for FREE

Stay informed with the latest T&D policies and technologies.

- Timely insights from industry experts

- Practical solutions T&D engineers

- Free access to every issue