CSA Z462 Arc Flash Training – Electrical Safety Compliance Course

Our customized live online or in‑person group training can be delivered to your staff at your location.

- Live Online

- 6 hours Instructor-led

- Group Training Available

Regular Price:

$249

Coupon Price:

$199

ANDOVER

—

High Lonesome Wind Farm powers Texas with 500 MW of renewable energy, backed by a 12-year PPA with Danone North America and a Proxy Revenue Swap, cutting CO2 emissions as Enel's largest project to date.

Context and Background

A 500 MW Enel wind project in Texas, supplying renewable power via PPAs and hedged by a Proxy Revenue Swap.

450 MW online; expanding to 500 MW in early 2020

12-year PPA with Danone North America for 20.6 MW

PRS hedge with Allianz and Nephila stabilizes revenues

Enel, through its US renewable subsidiary Enel Green Power North America, Inc. (“EGPNA”), has started operations of its 450 MW High Lonesome wind farm in Upton and Crockett Counties, in Texas, the largest operational wind project in the Group’s global renewable portfolio, alongside a recent 90 MW Spanish wind build in its European pipeline. Enel also signed a 12-year, renewable energy power purchase agreement (PPA) with food and beverage company Danone North America, a Public Benefit Corporation, for physical delivery of the renewable electricity associated with 20.6 MW, leading to an additional 50 MW expansion of High Lonesome that will increase the plant’s total capacity to 500 MW. The construction of the 50 MW expansion is currently underway and operations are due to start in the first quarter of 2020.

“The start of operations of Enel’s largest wind farm in the world marks a significant achievement for our company and reinforces our global commitment to accelerated renewable energy growth,” said Antonio Cammisecra, CEO of Enel Green Power, referencing the largest wind project constructed in North America as evidence of market momentum. “This milestone is matched with a new partnership with Danone North America to support their renewable goals, a reinforcement of our continued commitment to provide customers with tailored solutions to meet their sustainability goals.”

The agreement between Enel and Danone North America will provide enough electricity to produce the equivalent of almost 800 million cups of yogurt1 and over 80 million gallons2 of milk each year and support the food and beverage company’s commitment to securing 100% of its purchased electricity from renewable sources by 2030, in a market where North Carolina’s first wind farm is now fully operational and expanding access to clean power.

Mariano Lozano, president and CEO of Danone North America, added:“This is an exciting and significant step as we continue to advance our 2030 renewable electricity goals. As a public benefit corporation committed to balancing the needs of our business with those of society and the planet, we truly believe that this agreement makes sense from both a business and sustainability point of view. We’re delighted to be working with Enel Green Power to expand their High Lonesome wind farm and grow the renewable electricity infrastructure, such as New York’s biggest offshore wind projects, here in the US.”

In addition, as more US wind projects come online, such as TransAlta’s 119 MW project, the energy produced by a 295 MW portion of the project will be hedged under a Proxy Revenue Swap (PRS) with insurer Allianz Global Corporate & Specialty, Inc.'s Alternative Risk Transfer unit (Allianz), and Nephila Climate, a provider of weather and climate risk management products. The PRS is a financial derivative agreement designed to produce stable revenues for the project regardless of power price fluctuations and weather-driven intermittency, hedging the project from this kind of risk in addition to that associated with price and volume.

Under the PRS agreement, and as other projects begin operations, like Building Energy’s latest plant, High Lonesome will receive fixed payments based on the expected value of future energy production, with adjustments paid depending on how the realized proxy revenue of the project differs from the fixed payment. The PRS for High Lonesome, which is the largest by capacity for a single plant globally and the first agreement of its kind for Enel, was executed in collaboration with REsurety, Inc.

The investment in the construction of the 500 MW plant amounts to around 720 million US dollars. The wind farm is due to generate around 1.9 TWh annually, comparable to a 280 MW Alberta wind farm’s output, while avoiding the emission of more than 1.2 million tons of CO2 per year.

Related News

Related News

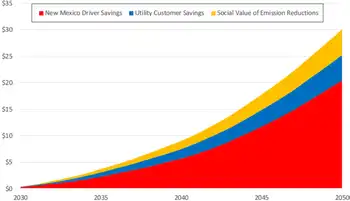

New Mexico Could Reap $30 Billion Driving on Electricity

New Mexico EV Benefits highlight cheaper fuel, lower maintenance, cleaner air, and smarter charging, cutting…

View more

Electricity Grids Can Handle Electric Vehicles Easily - They Just Need Proper Management

EV Grid Capacity Management shows how smart charging, load balancing, and off-peak pricing align with…

View more

U.S. Electricity Sales Projections Continue to Fall

US Electricity Demand Outlook examines EIA forecasts, GDP decoupling, energy efficiency, electrification, electric vehicles, grid…

View more

Wind has become the ‘most-used’ source of renewable electricity generation in the US

U.S. Wind Generation surpassed hydroelectric output in 2019, EIA data shows, becoming the top renewable…

View more

Alberta's Path to Clean Electricity

Alberta Clean Electricity Regulations face federal mandates and provincial autonomy, balancing greenhouse gas cuts, net-zero…

View more

A tenth of all electricity is lost in the grid - superconducting cables can help

High-Temperature Superconducting Cables enable lossless, high-voltage, underground transmission for grid modernization, linking renewable energy to…

View more

Sign Up for Electricity Forum’s Newsletter

Stay informed with our FREE Newsletter — get the latest news, breakthrough technologies, and expert insights, delivered straight to your inbox.

Electricity Today T&D Magazine Subscribe for FREE

Stay informed with the latest T&D policies and technologies.

- Timely insights from industry experts

- Practical solutions T&D engineers

- Free access to every issue